Gold Price Surge: A Safe-Haven Asset Amid Global Risks

Since the beginning of the year, gold is up 13%, surpassing a $3,000 per troy ounce mark- one of its best performances in history. The key growth drivers include:

- Inflation Hedge. Historically, gold has served as a safe-haven asset during periods of rising inflation. Tariffs imposed by the Trump administration have heightened fears of renewed rising prices. One-year consumer inflation expectations rose from 4.3% to 4.9% in March, while Fed officials have repeatedly stated that inflationary risks remain high.

- Geopolitics. Geopolitical tensions continue to escalate. The Trump administration has repeatedly expressed its readiness to intervene in military conflicts in the Middle East, which could lead to a further escalation of hostilities.

- Capital Flows Out of US Stocks. Since the beginning of the year, the US stock market has been declining. Investors are selling off US stocks amid the companies’ high valuations and concerns over slowing AI-driven revenue growth. This has resulted in a capital shift toward gold as investor risk appetite declines.

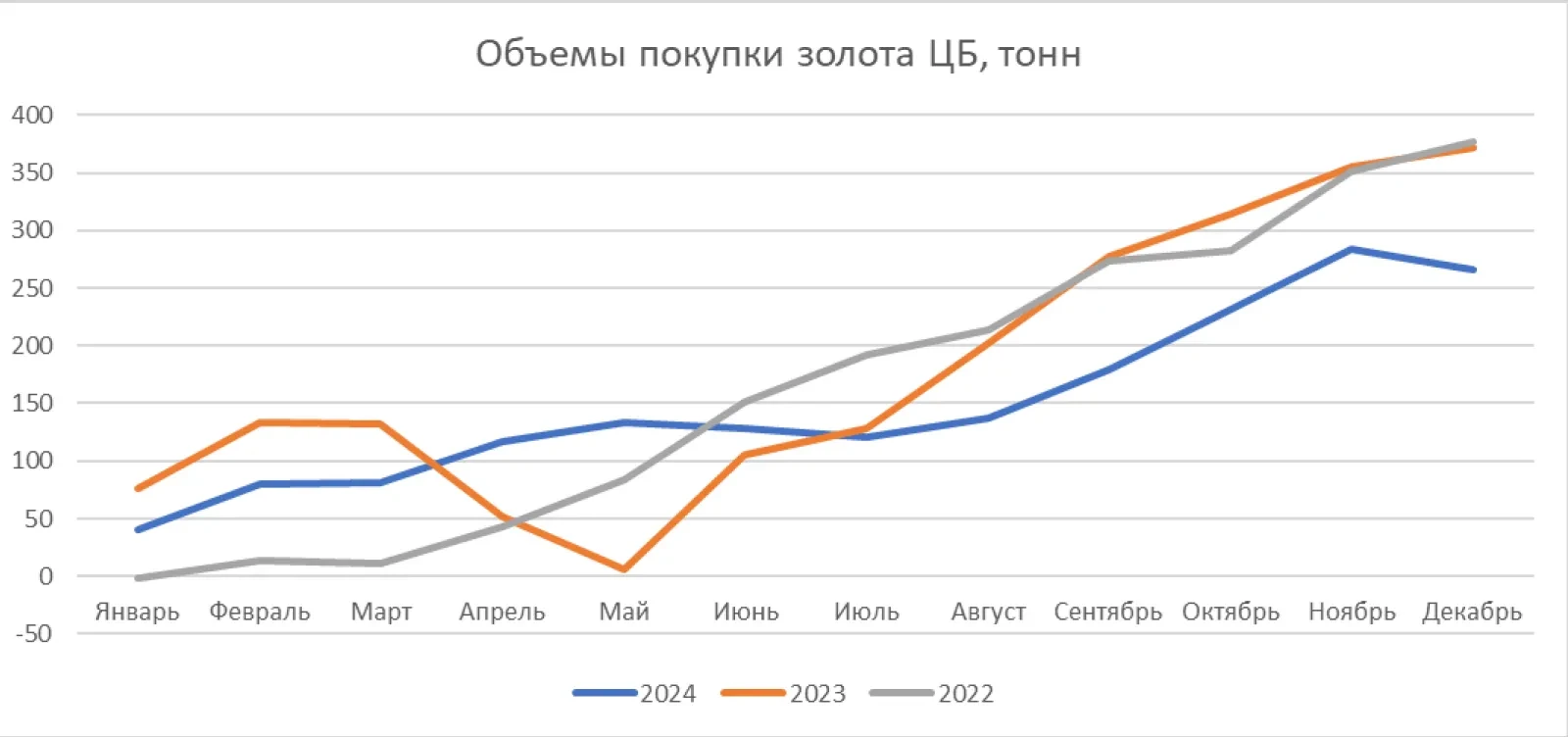

Despite the widespread belief that Central Bank demand for gold is increasing, the data suggests otherwise. In 2024, global central banks purchased a total of 265 tonnes of gold, compared to 371 tonnes in 2023 and 377 tonnes in 2022. Central banks are reluctant to buy gold at extremely high prices, leading to a slowdown in replenishment of gold reserves.

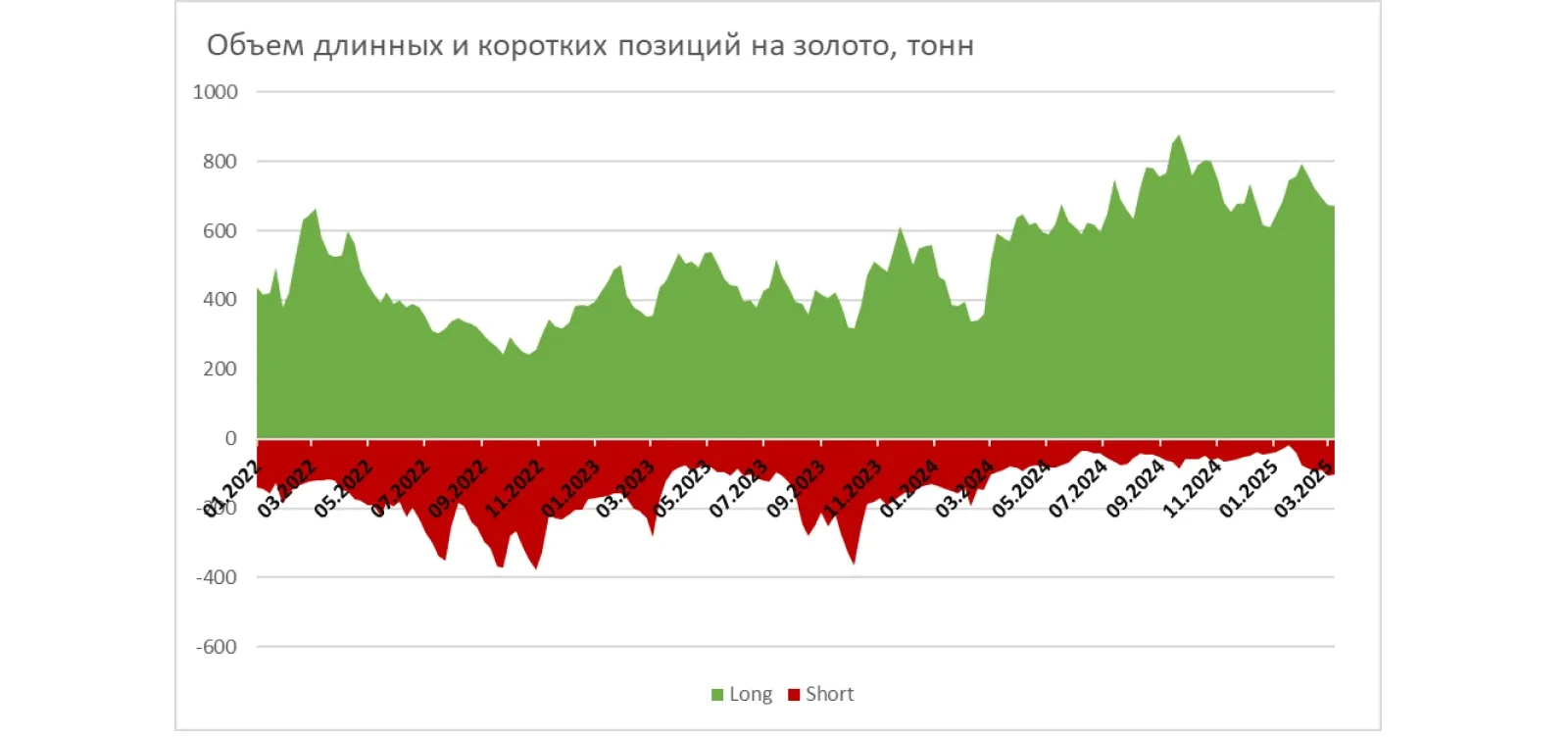

Since the beginning of 2025, the gap between long and short positions on gold has been narrowing. Bullish expectations for gold peaked in September 2024. The rapid 13% surge in gold prices since the beginning of the year reduces its potential growth, leading to more bearish expectations. However, as compared to early 2022, investor sentiment toward gold remains bullish, which may indicate a sustained long-term bullish trend.

Further gold price increase is likely to be limited. Fundamental factors such as supply and demand, central bank purchases, and the extremely rapid price surge since the beginning of the year suggest a potential slowdown in gold price growth. However, gold is still an extremely attractive asset to hedge the risks of rising inflation and geopolitical uncertainty. Trade wars between the US, China and the Eurozone are fuelling concerns over a resurgence of inflationary pressures, while increased military activity in the Middle East may signal escalating conflicts.

According to BCC Invest, the gold price in 2025 could rise to $3,200 in the baseline scenario and to $3,500 in the event of soaring inflation and escalating conflicts.

BCC Invest JSC

By clicking the “Confirm and Accept” button, you agree to the use of cookies in accordance with our Privacy Policy.