Gold: Second Quarter 2025 Results and Outlook

Record Growth in Gold Prices in Q2 2025

In the second quarter of 2025, the price of gold reached new historic highs amid increased demand and geopolitical tensions. In mid-April, prices exceeded $3,500 per ounce for the first time, nearly doubling compared to levels of around $1,800 three years ago. By the end of June, gold was trading around $3,275 per ounce, approximately 7% higher than at the beginning of the quarter and 25% higher than a year earlier. Thus, gold became one of the growth leaders: since the start of the year, it has gained about 25%, repeatedly setting new records. The main drivers of the rally were geopolitical instability and changes in monetary policy. Specifically, heightened geopolitical risks spurred demand for safe-haven assets: for example, in June, news of conflict in the Middle East triggered a price surge to $3,435 per ounce. Conversely, easing tensions and a moderately hawkish FRS stance temporarily cooled the market: after the FRS kept rates unchanged and a ceasefire was announced in the Middle East, gold retreated to $3,310–3,275 per ounce by the end of the quarter. Price dynamics were also affected by the weakening of the US dollar — the DXY index fell by nearly 10% in the first half of the year, which traditionally supports the value of gold as an alternative asset.

Unprecedented Demand from Central Banks

One of the key drivers of price growth was record-breaking purchasing behavior by central banks. According to the World Gold Council (WGC), from 2022 to 2024, central banks collectively purchased over 1,000 tonnes of gold annually. This is twice the average annual level (400–500 tonnes) of the previous decade. Such unprecedented demand from the official sector coincided with the sharp rise in metal prices, reinforcing the upward trend. Central banks' desire to increase the share of gold in reserves is explained by several reasons.

First, geopolitical and economic uncertainty persists, stemming from recent crises (from the pandemic to conflicts including the war in Ukraine), prompting the need to hold more reliable assets. Second, macroeconomic factors are significant: amid rising inflation and changing interest rate cycles, gold is viewed as a hedge against currency and interest rate risks. According to the WGC's 2025 survey, the vast majority of central banks cite gold's effectiveness during crises and its value-preserving role as the main reasons for increasing gold reserves. Gold is also valued for its ability to diversify portfolios and hedge against inflation. It is no surprise that 95% of central banks in the survey expect global gold reserves to increase over the next 12 months (compared to 81% the previous year). Notably, a record 43% of respondents plan to increase their own gold and foreign exchange reserves within the year—none reported plans to reduce them.

Source: World Gold Council, Central Bank Gold Reserves Survey 2025, June 17, 2025

The long-term strategy of regulators is also shifting in favor of gold. Around 76% of central banks forecast an increase in the share of gold in their reserves over a five-year horizon (69% in 2024). The flip side of this trend is the gradual de-dollarization of reserves: approximately 73% of respondents believe that in five years, the share of US dollars in global reserves will be moderately or significantly lower than today. This confirms the ongoing reallocation of reserves away from dollar assets in favor of gold and alternative currencies (euro, yuan, etc.). Another noteworthy trend is the growing professionalization of gold management: 44% of central banks now actively manage their gold reserves, compared to 37% a year ago. All these factors indicate continued strong official sector demand for gold. As noted by the WGC, central banks continue to recognize the benefits of holding gold in reserves, meaning their demand “is likely to remain healthy in the foreseeable future”.

Source: Source: World Gold Council, June 30, 2025

Investment Demand and the Market: New Phase

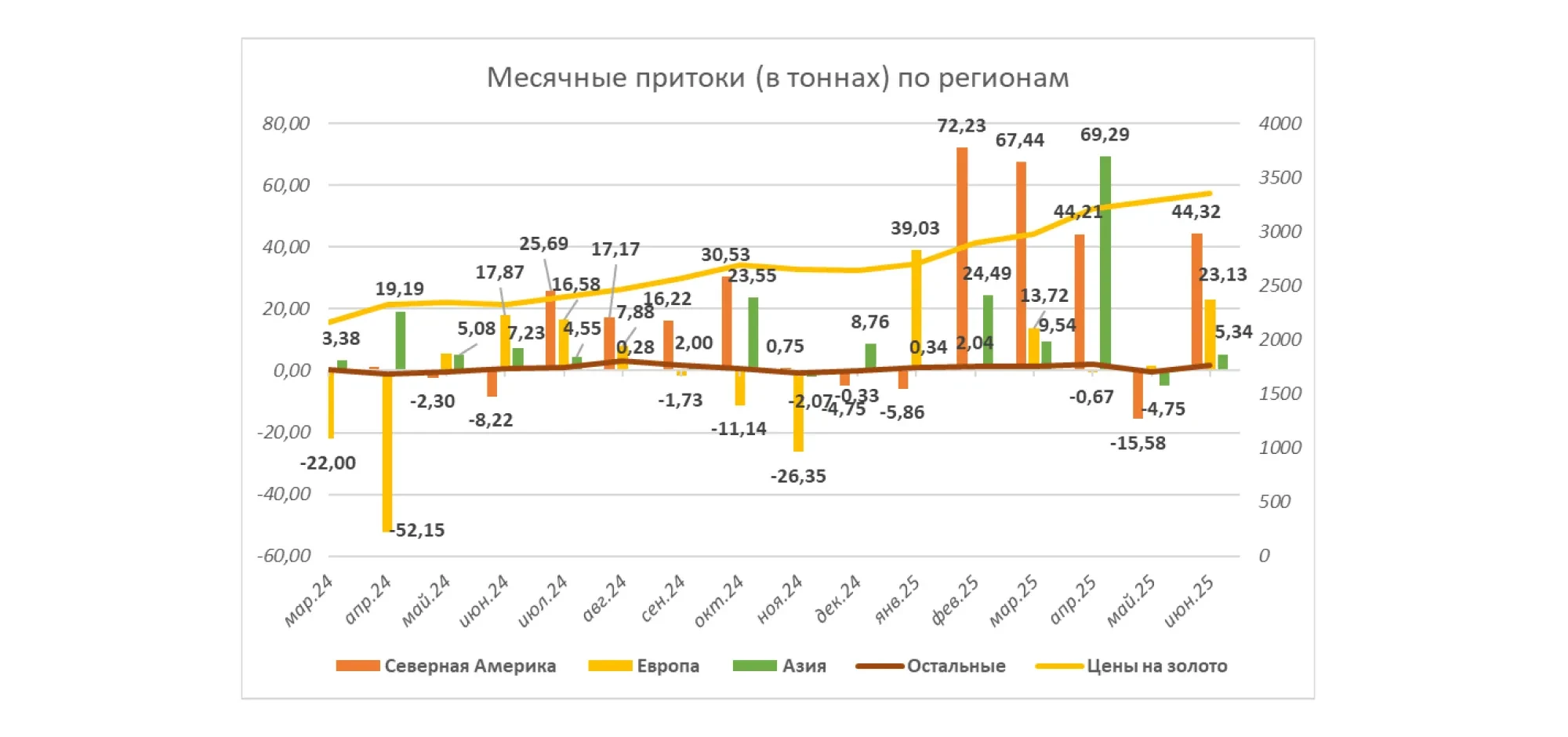

In addition to central banks, the second quarter saw a notable revival of interest from private investors and funds. After a period of relative calm in previous years, 2025 marked the return of net gold purchases through exchange-traded funds (ETFs) and futures. As of the end of June, total gold holdings in ETFs rose to 2,776 tonnes, up from 2,733 tonnes a month earlier, while speculative long positions on COMEX increased from 501 to 530 tonnes Investment in gold ETFs in developed countries resumed for the first time since 2020, although it was partially offset by selling in the futures market. A decline in real bond yields and expectations of imminent Federal Reserve policy easing have made non-yielding gold more attractive to investors. Indeed, in the second quarter, the U.S. central bank paused interest rate hikes, and markets began pricing in potential cuts, which traditionally supports precious metals. At the same time, moderate inflation (around 2.4% in the U.S. by summer) reduces the risk of aggressive monetary tightening, removing potential downward pressure on gold. In the physical market, demand from the jewelry sector remained relatively subdued, hovering near multi-year lows. However, the overall balance of supply and demand still favors the bulls.

Region | Total AUM (billion) | Inflow in funds (mln USD) | Asset volume (tons) | Demand (tons) | Demand (% of assets) |

North America | 196.3 | 7,826.0 | 1,857.2 | 72.9 | 4.09% |

Europe | 144.4 | 1,420.5 | 1,366.5 | 24.1 | 1.79% |

Asia | 34.5 | 7,403.2 | 320.7 | 69.9 | 27.87% |

Other | 7.6 | 334.1 | 71.5 | 3.6 | 5.23% |

Total | 382.8 | 16,983.9 | 3,615.9 | 170.5 | 4.95% |

Global inflow / Positive demand | 38,410.7 | 408.6 | 11.86% | ||

Global outflow / Negative demand | -21,426.8 | -238.2 | -6.91% | ||

Source: Source: World Gold Council, Q2 2025

Will Gold Continue to Rise?

Based on current trends, gold's outlook looks positive, although corrections are not excluded. Fundamental factors continue to support the market: central banks remain steady, large-scale buyers, continuing to diversify their reserves in favor of gold. Geopolitical risks are far from being resolved — from regional conflicts to trade disputes between major powers — so demand for a “safe haven” like gold is unlikely to weaken. Moreover, as global central banks shift toward monetary easing (rate cuts, halting policy tightening), the cost of holding gold decreases, which historically leads to rising prices for precious metals. At the same time, current price levels are near historic highs, so volatility may persist. In the event of a temporary improvement in geopolitical conditions or a strengthening of the U.S. dollar, price pullbacks are possible, as observed in late June. We have not revised our gold price target and continue to expect a return to $3,500 per ounce in the near term. For now, the overall trend remains upward: capital inflows from state institutions and investors provide strong market support. Overall, as of the end of the second quarter of 2025, gold has further strengthened its status as a reliable asset, and the outlook for the coming quarters remains positive.

BCC Invest JSC