Gold Breaks Out of Summer Lull

In the 2Q 2025, gold prices reached new all-time highs amid heightened demand and geopolitical tensions.

By early September, gold prices had reached $3,600 per ounce for the first time, nearly doubled as compared to levels around $1,800 three years ago. At the end of June, gold was trading at around $3,275 per ounce, which is about 7% higher than at the beginning of the quarter and 25% higher as compared to the year earlier. As a result, gold has become one of the top-performing leaders, gaining around 25% since the start of the year and repeatedly setting new records. The key drivers of this rally were global geopolitical instability and shifts in monetary policy.

In particular, heightened geopolitical risks fueled demand for safe-haven assets. In June, reports of the Middle East conflict triggered a price surge to $3,435 per ounce. Conversely, easing tensions and the Fed’s moderately hawkish stance temporarily cooled the market: after the Fed kept interest rates unchanged and a ceasefire was announced in the Middle East conflict, gold retreated to around $3,310–$3,275 per ounce by the end of the quarter. Price dynamics were also influenced by the weakening of the U.S. dollar – DXY index dropped nearly 10% in the first half of the year, which traditionally supports the value of gold as an alternative asset.

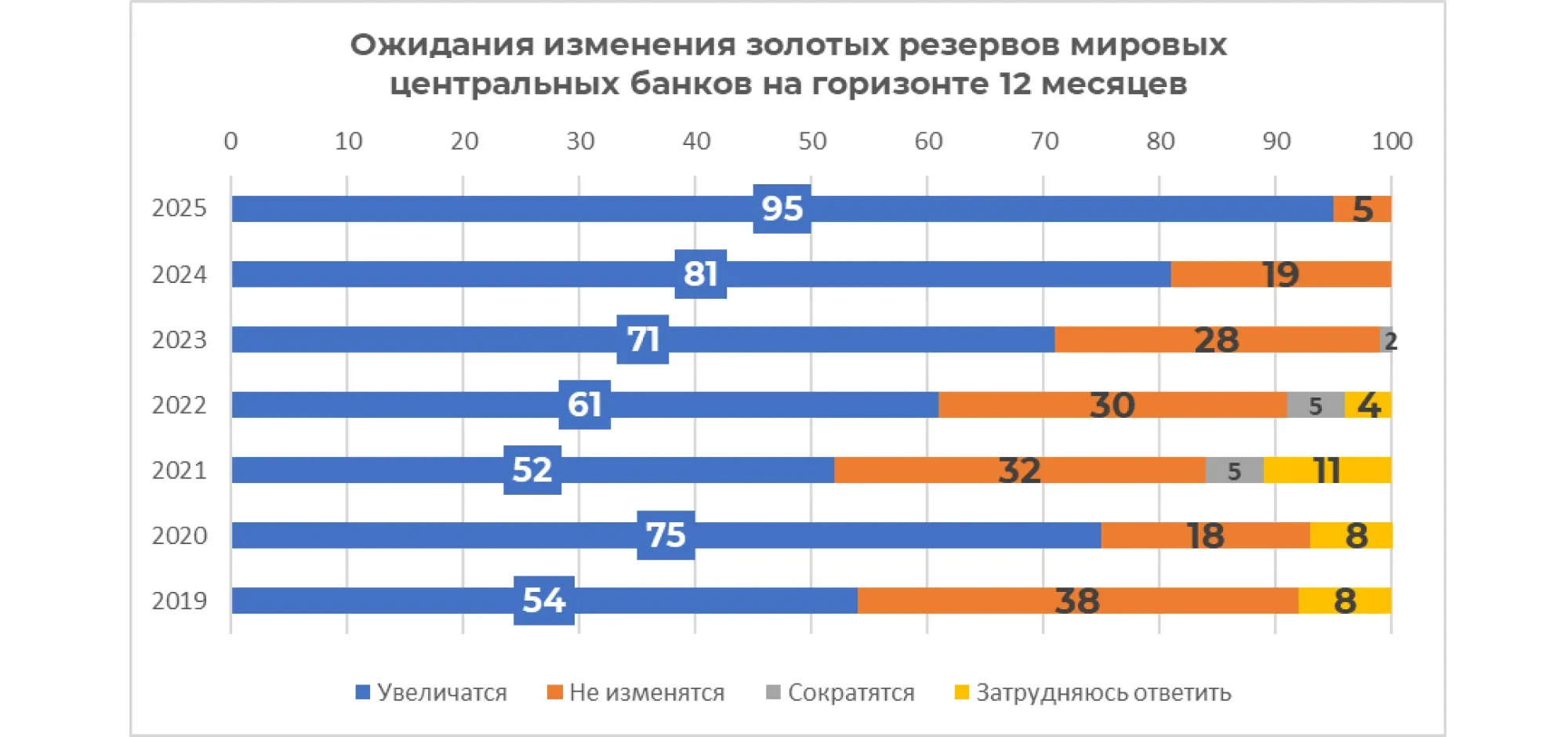

One of the key factors driving the price surge was record gold purchases by central banks. According to the World Gold Council (WGC), between 2022 and 2024, central banks purchased more than 1,000 tonnes of gold annually. This is twice the average annual volume (400–500 tonnes) purchased over the previous decade. This unprecedented demand from the official sector coincided with a sharp rise in metal prices, reinforcing the upward trend. Central banks’ efforts to increase the share of gold in their reserves are driven by several factors.

Source: World Gold Council, Central Bank Gold Reserves Survey 2025, 17 June 2025

First, the geopolitical and economic uncertainty originating from the crises of recent years (from the pandemic to conflicts, including the war in Ukraine) continues, driving to hold more reliable assets.

Second, macroeconomic factors play an important role: amid rising inflation and changing interest rate cycles, gold is seen as a hedge against currency and interest rate risks. According to the 2025 WGC survey, the vast majority of central banks cite gold’s effectiveness in times of crisis and its role in preserving value as the main reasons for increasing their gold reserves. Gold is also valued for its ability to diversify portfolios and hedge inflation.

It is not surprising that 95% of central banks surveyed expect global gold reserves to continue growing over the next 12 months (compared to 81% a year earlier). Notably, a record 43% of respondents plan to increase their own gold reserves within the year, while none of the participants indicated an intention to reduce them.

The long-term strategy of regulators is also shifting in favor of gold. Around 76% of central banks project a higher share of gold in their reserves over a five-year horizon (69% in 2024). The flip side of this trend is the gradual de-dollarization of reserves: approximately 73% of respondents believe that in five years, the share of U.S. dollars in global reserves will be moderately or significantly lower than it is today.

This confirms the ongoing reallocation of reserves from dollar-denominated assets toward gold and alternative currencies (EUR, CNY, and others). The growing professionalism in gold management is of additional interest: 44% of central banks now actively manage their gold holdings, compared to 37% a year ago. All these factors point to sustained demand for gold from the official sector. As the WGC notes, central banks continue to recognize the benefits of gold in their reserves, suggesting that demand is “likely to remain healthy in the foreseeable future”.

| Region | Total AUM (bn) | Fund inflows (mln USD) | Volume in assets (tonnes) | Demand (tonnes) | Demand (% of assets) |

| North America | 196,3 | 7 826,0 | 1 857,2 | 72,9 | 4,09% |

| Europe | 144,4 | 1 420,5 | 1 366,5 | 24,1 | 1,79% |

| Asia | 34,5 | 7 403,2 | 320,7 | 69,9 | 27,87% |

| Other | 7,6 | 334,1 | 71,5 | 3,6 | 5,23% |

| Total | 382,8 | 16 983,9 | 3 615,9 | 170,5 | 4,95% |

| Global inflows / Positive demand | 38 410,7 | 408,6 | 11,86% | ||

| Global outflows / Negative demand | -21 426,8 | -238,2 | -6,91% | ||

Source: World Gold Council (30 June 2025) for 2Q 2025

Based on the current trends, the outlook for gold remains favorable, though not without the potential corrections. The market is underpinned by the following fundamentals: central banks continue to be consistent, large-scale buyers as they diversify reserves in favor of gold. Geopolitical risks are far from being resolved – from regional conflicts to trade disputes between major powers – so demand for a “safe haven” asset like gold is unlikely to weaken. Moreover, when global central banks shift towards easing monetary policy (rate cuts and a pause in tightening), the cost of holding gold decreases, which historically leads to higher prices for precious metals. At the same time, current levels are at all-time highs, so volatility may persist. Temporary improvements in geopolitical environment or a stronger U.S. dollar could trigger price pullbacks, as seen at the end of June.

Gold has already reached its previously forecasted trajectory. At the beginning of the year, a rise to $3,000–$3,200 was expected, with prices expected to return to $3,500 per ounce by mid-year following a slight correction – but the market is already approaching $3,600. By year-end, prices are expected to reach around $4,000 per ounce, if the combination of inflows from government institutions and investors, soft central bank rhetoric, and heightened geopolitical uncertainty persists.

Overall, the trend remains upward – aggregate demand is providing solid support for the market, and according to the results of the 2Q 2025, gold has further reinforced its status as a reliable safe-haven asset.

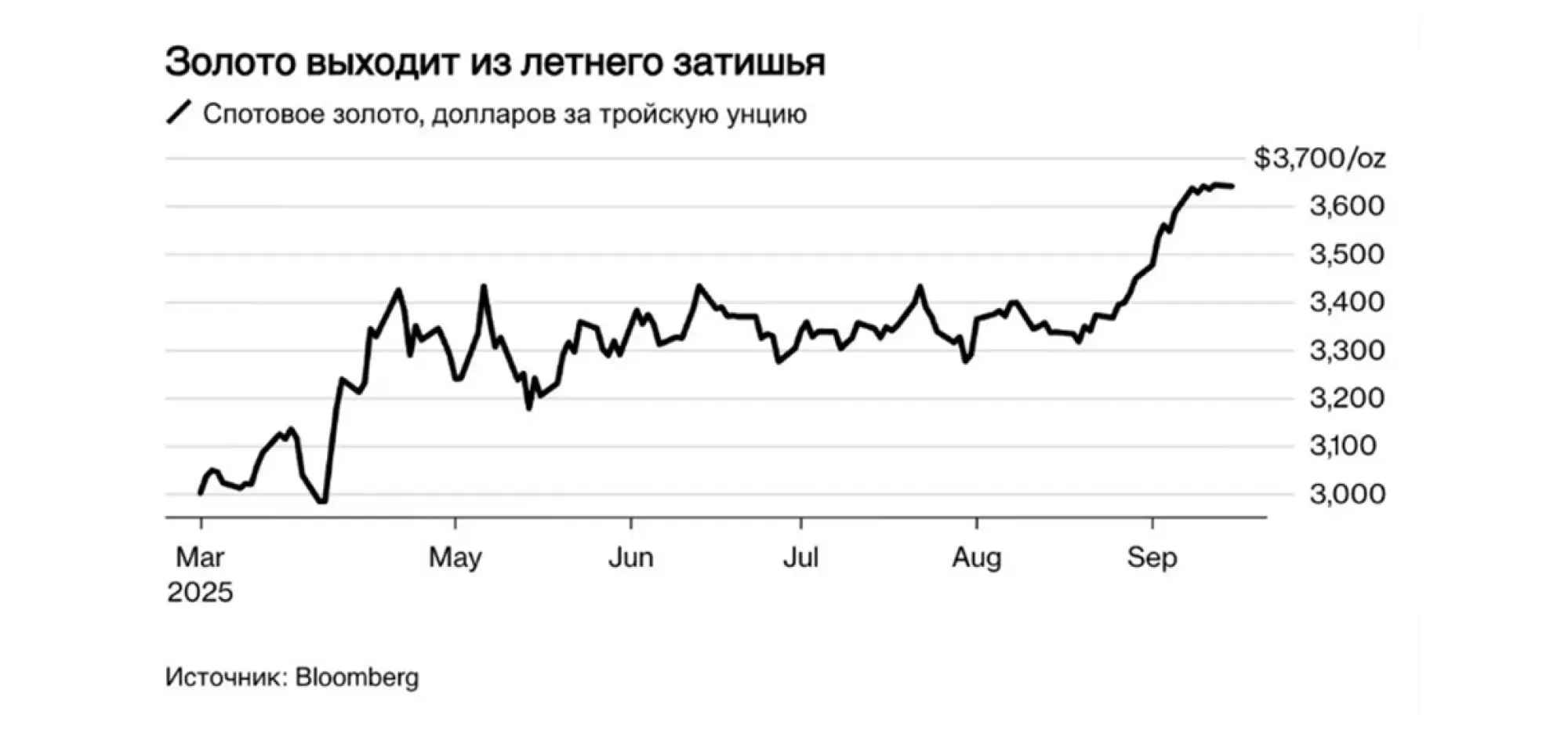

Amid expectations of a Fed rate cut and geopolitical tensions, gold rose, reaching above $3,700 per ounce. The combination of falling yields and search for a hedge is making gold the primary “cushion” for portfolios: as real yields decline, gold’s role in diversification only continues to strengthen. According to BCC Invest analysts, gold could reach $3,800-4,000 per ounce.

BCC Invest