Macroeconomic Review for October

October Highlights

- Kazakhstan’s economic growth continued in September, but for the first time this year its pace slowed.

- The main drivers of growth were increased oil production at the Tengiz field and higher budgetary stimulus through transfers from the National Fund.

- Inflation eased slightly due to a freeze on utility tariffs, but food prices rose at a record pace.

- The key driver of inflation remains high import dependence, especially on food products.

- Meanwhile, the trade surplus is shrinking amid falling oil exports.

- At the same time, the balance of services continues to improve, with exports growing faster than imports.

- Despite these trends, the tenge unexpectedly strengthened in October as the National Bank intensified its sterilisation of tenge liquidity.

- Economists expect the final two months of 2025 to bring a gradual slowdown in growth and a narrowing of the trade surplus. Monetary measures should help contain inflation within forecast ranges, while the exchange rate is expected to remain stronger than baseline projections.

Economic Growth

In October, data on Kazakhstan's economic growth for January–September 2025 were published. According to this government data Kazakhstan’s GDP grew by 6.3% year-on-year. The growth of key sectors of the economy, reflected in the short-term economic indicator, amounted to 9.1%, marking the first slowdown in pace since the beginning of the year.

The highest growth was recorded in the transport and storage sector, where output increased by 22.2%. The high growth rates in the sector are associated with an increase in freight volumes through Caspian ports (+32.8%), as well as the growth of gas, oil, and water transit through pipelines (+15.9%), especially in the Mangystau region.

Construction also grew rapidly (+14.9%), with Astana accounting for a striking 41.8% increase and nearly 15% of total national construction output.

Mining and trade expanded by 9.3% and 8.8%, respectively. Oil production rose 13.2%, reflecting strong performance in major energy projects.

Growth in trade was supported by higher prices for imported goods and rising consumer demand amid population growth.

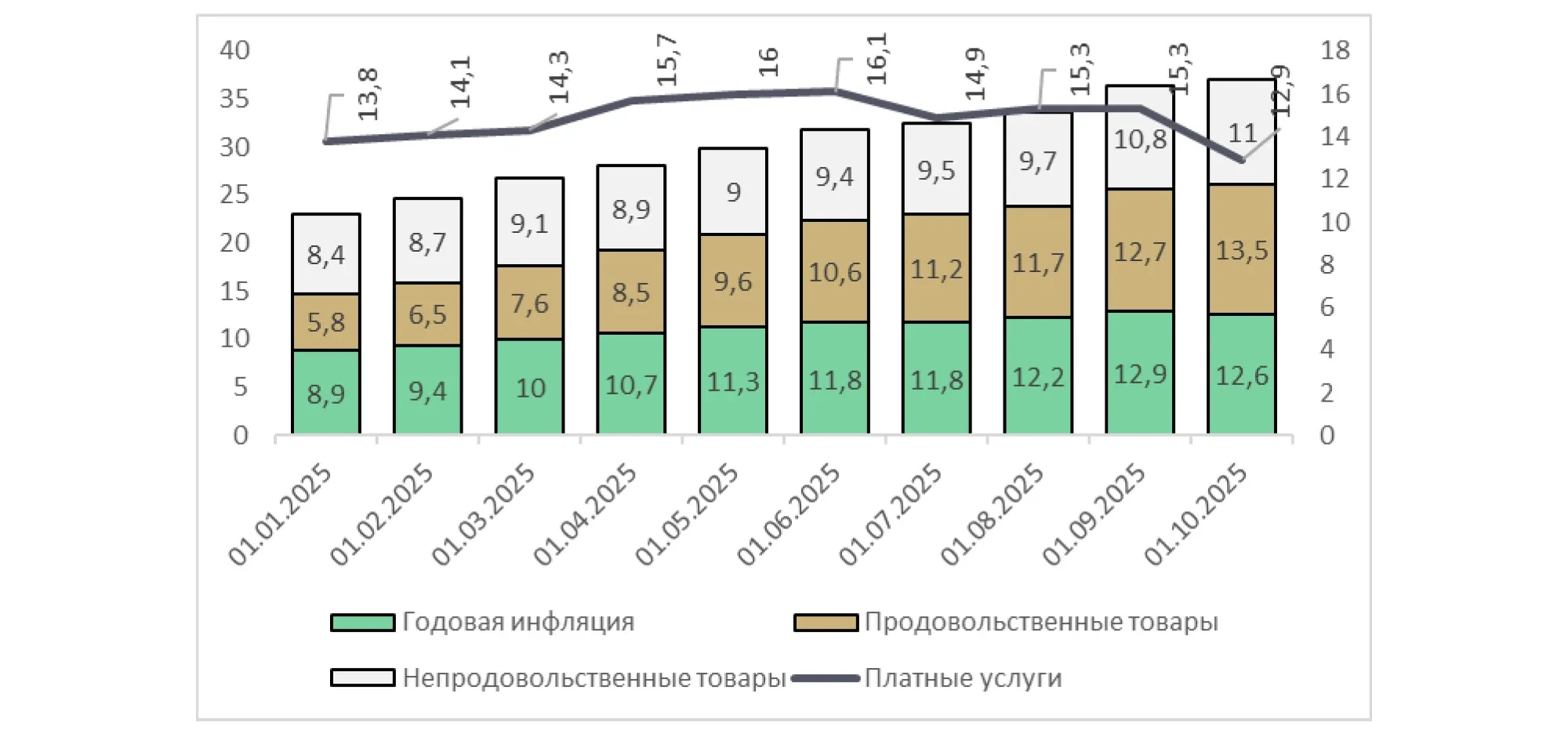

Inflation

Annual inflation reached 12.6% in October 2025, while monthly inflation stood at 0.5%. This is slightly below baseline forecasts. In September, inflation had been 12.9% year-on-year and 1.1% month-on-month.

The main upward pressure came from food prices, linked to the growing share of imported goods and sustained cost pressures.

A restraining factor was the reduction of utility tariffs due to the price freeze until the end of the first quarter of 2026, which helped to slightly slow down the overall pace of price growth.

Figure 1. Actual and projected inflation in 2025

Source: BCC Invest calculations based on data from the RoK ASPR BNS

In October, the National Bank’s Monetary Policy Committee raised the base rate to 18.0% to curb inflationary pressure and stabilise expectations. At the same time, the regulator tightened lending conditions, which is expected to be reflected in price dynamics and consumer market activity in the coming months.

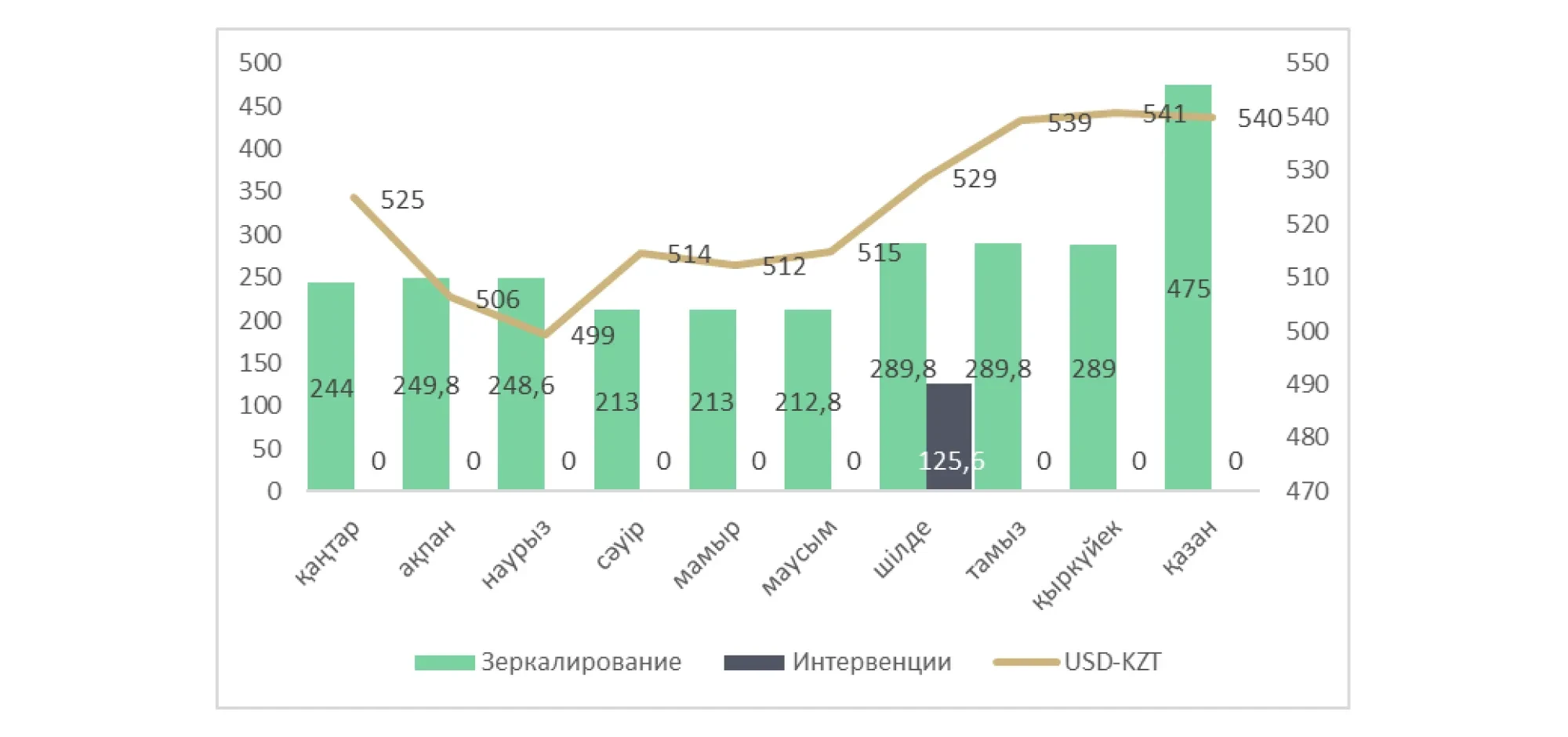

Tenge Rate

According to the Kazakhstan Stock Exchange (KASE), the tenge ended October at ₸529.96 per USD. The monthly average rate was ₸539.9 per USD, slightly stronger than in September (₸540.74 per USD).

The National Bank did not conduct direct foreign exchange interventions but sterilized ₸475 billion of liquidity through mirror operations — up sharply from ₸290 billion in September — a move that contributed to the tenge’s strengthening.

The average annual exchange rate for 2025 remains within the forecast range at ₸522.1 per USD, compared with the baseline projection of ₸526.8 per USD. So, the deviation is only ₸4.7

Overall, October saw a firmer tenge and renewed demand for the national currency. The exchange rate dynamics were in line with the baseline scenario.

In November, the National Bank plans to continue liquidity sterilisation through gold operations worth about ₸475 billion, which should support the exchange rate. However, the ongoing decline in the trade surplus will continue to exert downward pressure on the tenge.

Figure 2. Dynamics of the USD/KZT exchange rate in 2025

Source: BCC Invest calculations based on data from the RoK ASPR BNS

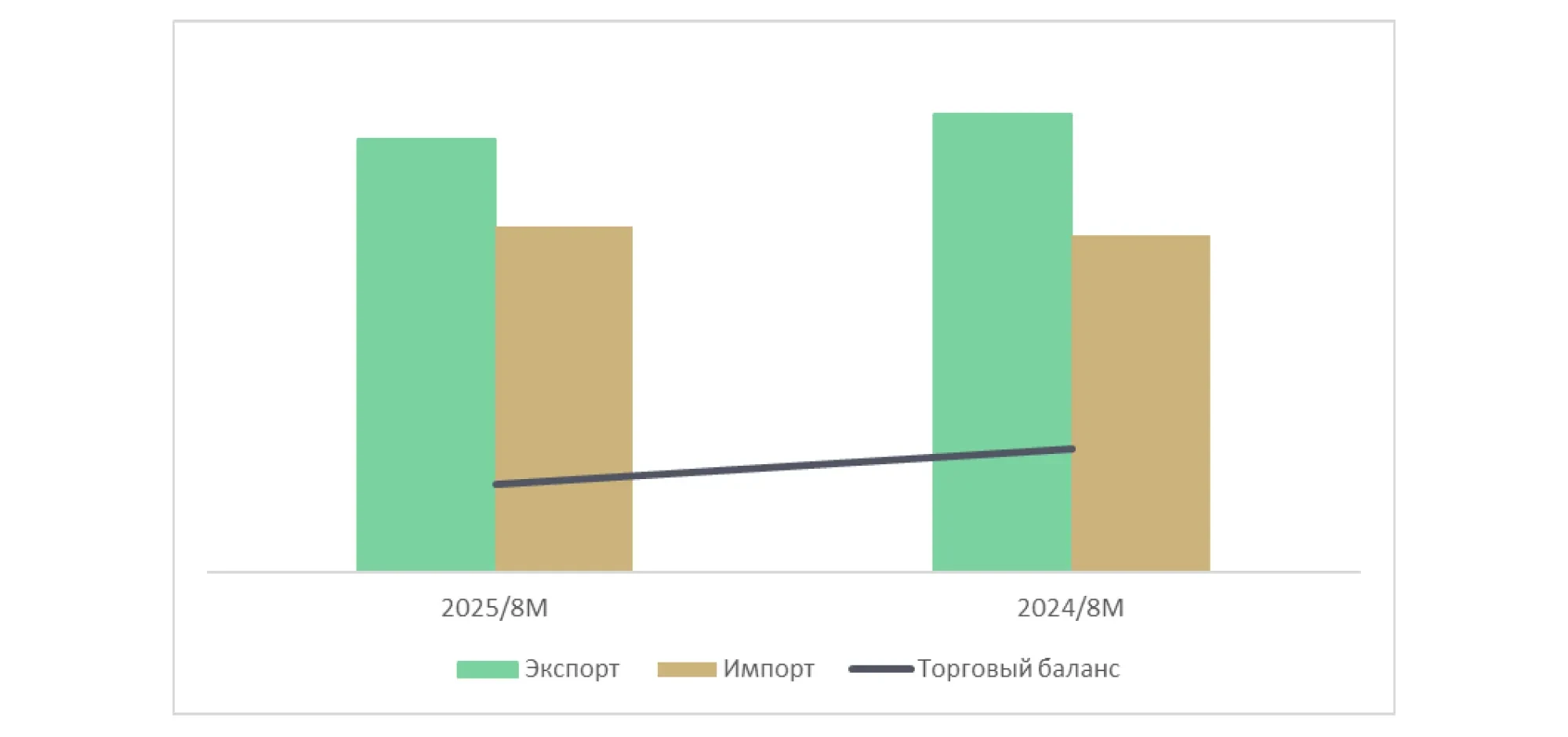

Trade and External Economic Balance

In October, new data on the current account was published — an indicator reflecting the difference between how much foreign currency the economy earned and how much it spent abroad. This indicator traditionally remains negative, as a significant portion of foreign currency revenue from oil production is paid to foreign investors.

By the end of the first half of 2025, the current account deficit deepened to USD -3.9 billion, compared to USD -1.9 billion a year earlier. The main reason lies in the dynamics of one of its key components, the trade balance (the difference between exports and imports), which, although still positive, is gradually narrowing.

Kazakhstan’s trade balance has traditionally shown a surplus due to substantial oil export volumes. However, in 2025, oil exports generated less foreign currency revenue. According to data for January–August, exports continued to decline (–5.7%) while imports increased (+2.8%) year-on-year. As a result, the trade surplus decreased by 30% to USD 8.9 billion. Excluding oil, the trade balance amounted to –USD 15.7 billion, compared to –USD 14.9 billion a year earlier.

The shrinking surplus is putting additional pressure on the tenge exchange rate and has become one of the factors behind its weakening.

Figure 3. Trade results for January–August, USD million

Source: BCC Invest calculations based on data from the RoK ASPR BNS

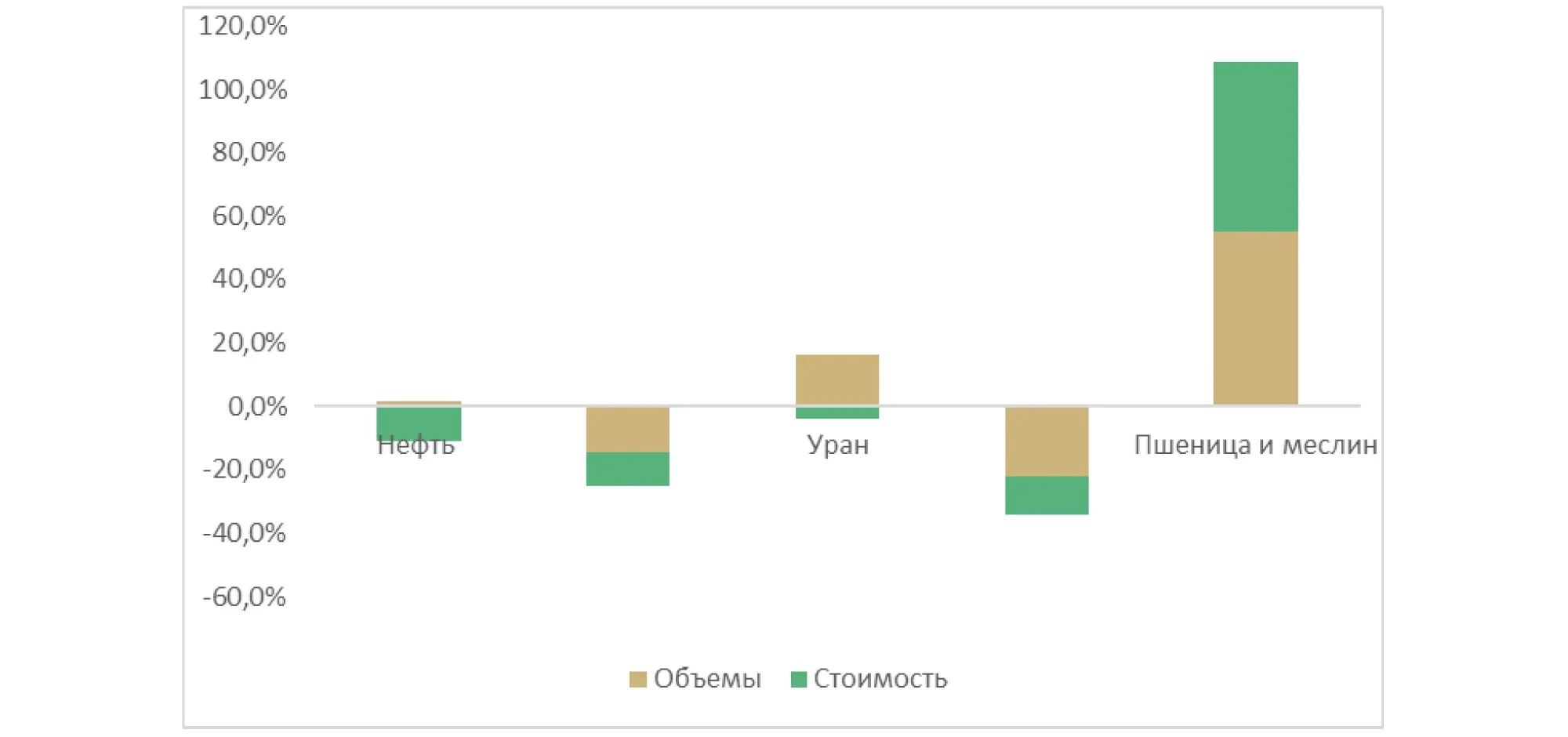

The overall decline in export volumes was primarily due to reduced deliveries of oil, copper, and uranium — Kazakhstan’s main export commodities. Together, they accounted for 65% of total exports, compared to 69% in the same period last year. At the same time, the share of food products in exports increased to 8.4%, and that of other finished goods and semi-finished products to 2.0%, while the share of fossil raw materials fell to 62.5%.

Notable development was the sharp growth in wheat exports, which reached USD 990 million for the first time — 54% higher than in the first eight months of last year.

Figure 4. Growth rates of key export commodities for January–August, USD million

Source: BCC Invest calculations based on data from the RoK ASPR BNS

In September, the global market saw strong unmet demand for nuclear fuel, and Kazakhstan’s exports of nuclear semi-finished products increased by 16.2%. However, their value fell by 3.8%, indicating significant discounting in uranium exports.

Oil exports also declined by 11.3% amid stagnating global oil prices in August and September. It is noteworthy that exports fell despite a significant increase in oil production — 58.5 million tons of crude oil were produced during the same period, 15.0% more than in January–August last year.

According to our estimates, total exports for 2025 will amount to USD 78.2 billion, 4.1% lower than in 2024, while imports are expected to increase by 4.4% to USD 62.4 billion, continuing steady growth. As a result, the trade balance may reach USD 15.8 billion, which is 27.7% lower than in 2024.

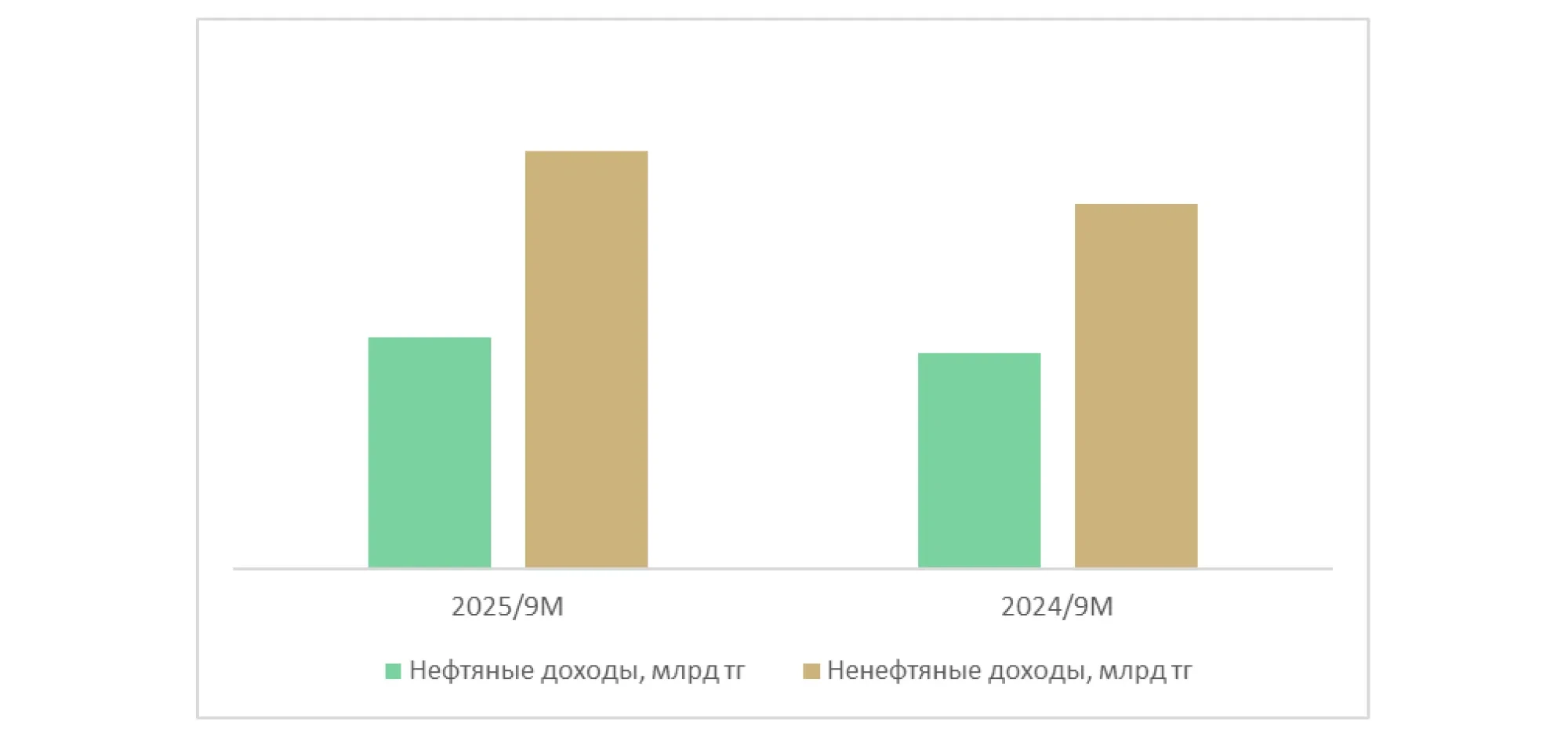

Republican Budget and Public Debt

The state of the republican budget for the reporting period improved compared to January–September last year. Revenues grew faster than expenditures — by 11.7% and 7.5%, respectively. Meanwhile, the balance of transactions with public assets remained positive, although it declined by 29% year-on-year, and the volume of budget loans issued increased by 13.7%.

As a result, the overall deficit decreased by 12.1%, while the non-oil deficit remained almost unchanged. Oil-related budget revenues (transfers from the National Fund and export duties on oil) rose by 7.4%, while non-oil revenues grew faster — by 14.3%. This indicates that the share of oil revenues in total government income has slightly decreased, at least over the January–September period.

Figure 5. Budget revenues, KZT billion

Source: BCC Invest calculations based on data from the State Revenue Committee, RoK Ministry of Finance

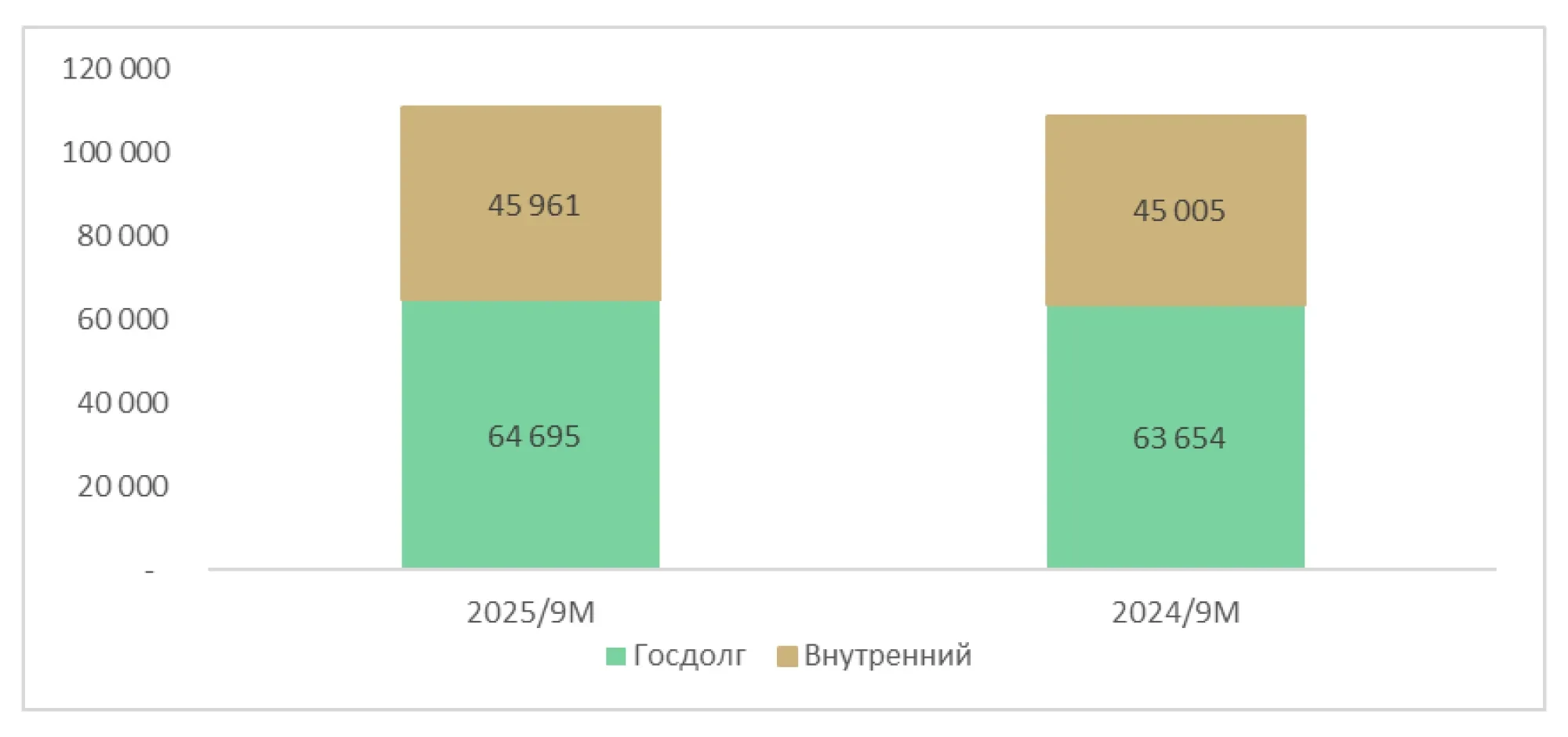

Public debt increased by 1.6%, with external debt up 5.6% and domestic debt up 2.1% year-on-year. Although Kazakhstan’s public debt remains relatively low, the share of debt servicing costs in total budget expenditures remains high at 13%, continuing the trend of the past five years, during which the debt burden on the budget has gradually increased (in 2021, it accounted for about 8% of total spending).

Figure 6. Public debt, USD million

Source: BCC Invest calculations based on data from the State Revenue Committee, RoK Ministry of Finance